Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Less than three months after presenting her first budget, Rachel Reeves is running into treacherous financial waters as the UK’s rising borrowing costs erode room for her strategy.

There is now a real risk that the Chancellor will be forced to impose tighter monetary policy as soon as March, when the Office for Budget Responsibility presents its forecasts, as he seeks to meet his self-imposed budget constraints.

In light of Reeves’ claims that the situation is detrimental to the Labor government, its October Financial statements It marked a landmark effort to “clean the slate” on UK budget issues.

The central problem is a constant get up The cost of government borrowing, in the UK and around the world. The United States has been a central factor in global bond selling in recent months, driven in part by expectations that tariffs imposed by US President-elect Donald Trump will boost inflation.

But the UK has been hit particularly hard by fund managers’ concerns the economy A “stagflation” period may enter, where persistent price pressures prevent the Bank of England from lowering interest rates to raise it.

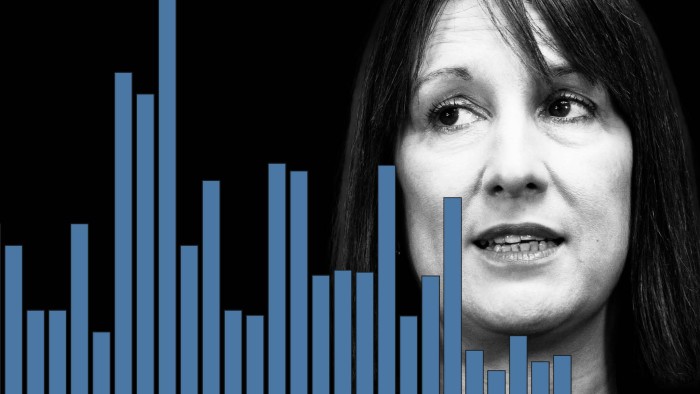

Coupled with a rise in debt sales expected after the Budget, fears of recessionary inflation have helped send the UK’s 10-year borrowing costs to their highest level since the 2008 global financial crisis and its 30-year borrowing costs to their highest this century. It has triggered bouts of weakness for sterling.

“The mix of pressures on both gilts and currencies suggests that markets are getting worried about a UK recession or financial events,” said Jim McCormick, macro strategist at investment bank Citi.

The high cost of borrowing has direct implications for Reeves’ budget plans, increasing interest payments that already exceed £100bn a year.

He has set a target of balancing the current budget excluding investment expenditure by 2029-30. October forecasts from the Office for Budget Responsibility, the fiscal watchdog, suggested Reeves That would meet the rules with a margin of £9.9bn remaining in the year.

But high interest costs are jeopardizing his goals. Long-dated gilt yields have continued to rise in recent weeks, with the 10-year gilt yield hitting as high as 4.82 percent on Wednesday, the highest since 2008.

Ruth Gregory, economist at consultancy Capital Economics, said the movement seen so far would be enough to clear headroom against the current budget rules, with the Treasury now on track to break the rules by around £1 billion.

This estimate is derived from the BoE’s benchmark interest rate and market-based expectations for the 20-year gilt yield.

“No one should be in any doubt that meeting revenue norms is non-negotiable and that the government will have an iron grip on public finances,” the Treasury said on Wednesday. “Only OBR forecasts can accurately predict how much headroom the government has – anything else is pure guesswork.”

The OBR forecasts on March 26 will also set a revised outlook for growth, which will also have a significant impact on public finances. GDP readings at the end of last year were weaker than expected and the BoE estimates that the economy has failed to grow in the last three months of 2024.

The weak data undermined the OBR’s October forecast for economic growth of 2 per cent in 2025, analysts said.

But the impact of GDP movements on borrowing depends on whether the OBR judges whether the economy can bounce back and cover the deficit later in Parliament, or whether it decides whether output has suffered permanent damage.

A downgrade by the OBR would represent a further blow to the Treasury and public finances from the perspective of UK productivity and potential growth.

The UK’s fiscal outlook worsens as the government prepares for the next phase of its multi-year spending review, the outcome of which is expected in June.

The Treasury set its overall Whitehall departmental spending envelope in the October Budget, with daily spending rising by 3.1 per cent from 2026-27 to 2025-26 before falling to 1.3 per cent from 2026-27.

Detailed plans are laid out for the initial years; The cost review is now looking at next year. Officers have signal If Reeves needs to make an overhaul of fiscal policy this spring, it will likely come through a tougher spending plan rather than an initial tax hike.

That’s because he has promised to hold only one “fiscal event” per year, which will be around the time of the tax changes and won’t take place until the autumn.

Restoring headroom to October levels of just under 10 billion pounds through tougher spending plans would mean curbing real-term growth in day-to-day department spending from 1.3 percent a year to just under 1 percent, said Ben Zaranko, associate director of the Institute for Fiscal Studies think-tank.

But analysts fear that if the selloff in the bond market continues, Reeves may be forced to go further to reduce financial credibility. Such measures could require tax increases and front-load spending restraint, and not just promises of greater discipline late in Parliament.

“Reeves may soon face a nasty choice of breaking his fiscal rules or announcing more tax increases and/or spending restraint at a time when the economy is already weak,” Gregory said in Capital Economics.

The chancellor is aiming to focus on a “pro-growth” narrative in the coming weeks and that faster economic expansion will pay dividends in terms of public finances.

Reeves is preparing to travel to China this week as he looks for ways to boost the economy.

But hopes for a strong turnaround in GDP growth can be easily misplaced. With government bond prices falling, investors have warned that efforts to establish a strong fiscal base for the current parliament are at risk.

Pooja Kumra, UK rates strategist at TD Securities, said Reeves had “no room left, as selling has been relentless since October”.

Data Visualization by Keith Frey